By Linda Schmid

In the last quarter of the year, predictions were made by many industry and economic experts that 2023 was going to be a let-down after the flurry of construction activity that was 2022. It’s time to check on that prediction and see if it holds up under scrutiny…What is the state of the industry? Also, how is the rest of the year expected to pan out?

In the Foreground

Wayne Troyer, Acu-Form, says that from his viewpoint, the economy is good and business is still going strong. He doesn’t expect that to change in 2023.

“We see a lot more people using metal on their buildings. They are thinking long-term on the materials they use to build,” he says. That can only bode well for those in the roll-forming business.

Chandler Barden, President of Cidan Machinery also sees an economy full of possibility. “From our perspective, the economy has remained in a strong enough position for expected growth.”

He continues: “With changes in the economy and populations moving, we may see a larger growth variance across regions of the country.”

Ken McLauchlan of MetalForming, LLC says that he has heard of some slowing in specific markets, but for the most part, “companies that are diverse, manage the process, and are willing to accommodate project demands continue to have great backlogs.”

McLauchlan also says that there are several markers for the industry that inform you how the industry is doing: building permit applications, industry reports on material usage, and sales history — both internally and externally — compared to current sales.

Interest Rates

Troyer says that he, like many others, is paying a lot of attention to interest rates. “Hopefully The Fed realizes that raising interest rates too much will hurt the economy.”

McLauchlan believes that while the industry expected to see the increasing prime rate inhibit market growth, instead it has changed the focus of work from new builds and new roofs to renovations and retrofits. Further, with the increases in material costs, more projects will take the long-term costs of the materials chosen into consideration and some will choose the more durable materials.

Ben Johnston, COO of Kapitus, a provider of financing for small- and medium-sized businesses comments, “Higher interest rates are cooling the real estate market across the country, but we continue to see strong credit demand from contractors as a shortage of affordable housing, coupled with low unemployment rates, generate demand for new housing stock.” He also sees homeowners who are locked into lower rate mortgages choosing to stay in their homes rather than selling and repurchasing in a higher rate market. These homeowners are looking to renovate existing housing stock, driving demand for contractors.”

Since spring of 2022, Johnston has seen a tightening in credit, however, which accelerated after the failures of SVB and Signature Banks. As banks become more cautious, many quality applicants, often small businesses, are unable to obtain the financing they need.

Perhaps tighter credit explains why Sean Shields of the Structural Building Components Association (SBCA) sees that single-family housing construction has returned to 2019 (pre-COVID) levels. He notes that many component manufacturers who were in a position to pivot to multi-family projects actually saw an increase early this year as near-record numbers of large projects got underway.

High-end earners who will sometimes move forward with projects regardless of the economic situation have continued to invest in real estate and home improvement.

The Economy’s Impact on the Industry

For many, the slow start to the year is providing the opportunity to retool and retrain.

“Production equipment that has been on backorder for 12 months or more is being delivered and installed,” Shields explains. “Personnel have to be trained on these new systems, and the current conditions are favorable to getting this new capacity up and running.”

Due to the current slowdown, lumber costs have been relatively low for most grades and sizes. MSR lumber is still difficult to source in many areas of the country, though, impacting products such as floor trusses and long span roof trusses.

However, it appears that not all construction niches are equal. Rob Haddock, CEO of S-5!, says that while residential construction has taken a geographically varied hit, other sectors are doing well.

“The commercial/industrial space is still reasonably robust, especially in manufacturing and data center related construction. The agricultural marketplace is on stable ground, pardon the pun,” Haddock says.

“Obviously, the economy has dampened real property commerce because of interest rate increases, but the uncertainty of economic stability going forward has played the greatest role in dampening the construction economy,” Haddock continues.

Keith Dietzen, CEO of Keymark, says that it’s a bit of a surprise how strong the post-frame and roofing industries have remained while interest rates have gone from near zero to the highest in many years.

He hasn’t seen that the Federal Reserve’s interest rate adjustments have affected business much currently. “My customers all report a very strong book of business,” he says.

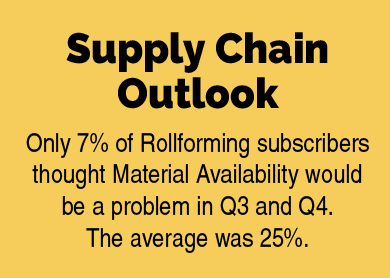

On another note, Barden sees that the supply chain situation is more manageable than it has been since 2020.

Troyer, however, is surprised to see that lead times for many components are still an issue.

On the Horizon

Tom Bowne, Chief Economist for the Freedonia Group (a division of MarketResearch.com, Inc.) has this to say regarding the industry’s progress: “We expect that residential construction activity will face a number of headwinds in 2023. As the Federal Reserve maintains its tighter monetary policy in an effort to keep expectations of future inflation from rising, mortgage interest rates will remain elevated, constraining housing demand. Smaller regional banks are likely to be less eager to make construction loans while these banks’ balance sheets are under increased scrutiny. That tighter lending environment will weigh on builders’ and contractors’ ability to finance projects.

“Later in the year, however, there is a chance that the Federal Reserve may ease monetary policy somewhat, offering some relief for mortgage lending,” Bowne says.

The other factor that will likely provide a boost to new construction as 2023 progresses according to Bowne is the aforementioned lock-in effect of existing homeowners with low mortgage interest rates retaining ownership. The lack of available houses will create new home construction demands for newly formed households.

The Labor Pool

Shields says that component manufacturers as a group expect the last half of 2023 to pick up. There is concern that many projects will be started within the same time frames, thereby straining supply chains and causing volatility in the lumber and steel markets. Further, hiring and training enough help to service a spike in demand could be problematic.

Barden believes that hiring enough labor is going to be an ongoing challenge for the foreseeable future.

“We see technology developing quickly to address these shortages,” Barden states. “The industry is pushing innovation in manufacturing to address this, and companies are investing in it, using more software to increase efficiency of their current workforce. Although this has been in the news for general manufacturing for years, it is quickly penetrating into the architectural sheet metal industry.”

Dietzen concurs that the labor shortage will continue to be problematic. He also sees automation as the answer.

“One of the most effective ways to address the labor challenge is to use software systems that can automatically generate necessary information that otherwise would require many hours of toil from team members who are already more than busy,” Dietzen says.

Trouble Ahead?

These concerns may be inapplicable, at least in the short term however, as Johnston warns that the SVB and Signature Bank failures have made everyone more cautious and if interest rates continue to rise, participation by those paying the bills may dissipate. More likely they will continue to build and invest, but they will be looking for price concessions and better overall terms Johnston says.

Johnston’s group sees trouble ahead for the commercial market as remote work becomes a permanent fixture in American life and many long-term leases expire.

Bowne feels the outcome of that trend is uncertain. He put it this way: “Office construction is expected to see below-average activity for a few more years as businesses continue to sort out staffing arrangements (in-person vs. hybrid) and their need for space to handle their personnel.”

He expects that the non-residential construction markets in general may face a bit of a downturn similar to the residential market later this year based on the difficulty in obtaining construction financing.

“Activity in retail building construction will be dampened if consumer confidence and overall economic activity weaken during the middle part of 2023,” Bowne says.

However, he does offer some hope for light manufacturing: “Construction of light manufacturing facilities will continue to be aided by efforts to improve supply chains, which could induce some re-shoring of manufacturing activity,” he concludes.

Over-All Advice

Troyer thinks we are through the worst of industry challenges and exhorts everyone to stay positive and keep up the good work. Quality and service are always in demand.

McLauchlan emphasizes identifying allies in the industry and partnering with companies that align with your company goals and needs. Further, with greater automation, people with training, service, and support for that technology are going to be needed. “Look for companies with long-term market presence,” he advises.

The market continues to see increased interest in energy efficiency, making a good case for Haddock’s advice, which is to be proactive and provide a “Plan B” for your company in case your usual revenue source takes a dip. For example, get involved in solar photovoltaic products.

Two trends that Dietzen has observed seem to bode well for the future: More and more roofing contractors are adding metal roofing to their service menu and consumer demand for barndominiums is growing. “There is real opportunity in these markets,” Dietzen reveals.

Troyer states that with the price of crops and dairy, the ag side is getting stronger and stronger.

Maybe metal roofing, barndominiums, and ag buildings are more good Plan B options.

Barden’s advice for navigation of 2023: “Invest in your business to build a platform for scale and growth, otherwise the ramp-up time for these projects can put you in a position where you are chasing your competitor.”

He adds that everyone can use a bit of support: “Get involved with the industry associations for education, networking, and leading indicators on opportunities and risks.” RF

{kind=link}